When last I mentioned isoquants, I suggested that the 1000-isoquant would be an important level for the next few months. A common thread of the commentary (after the etch-a-sketch comments) on ZH today was the difficulty of following the chart. So today I present two short segments involving the 1000-isoquant level to show why I think it has some importance.

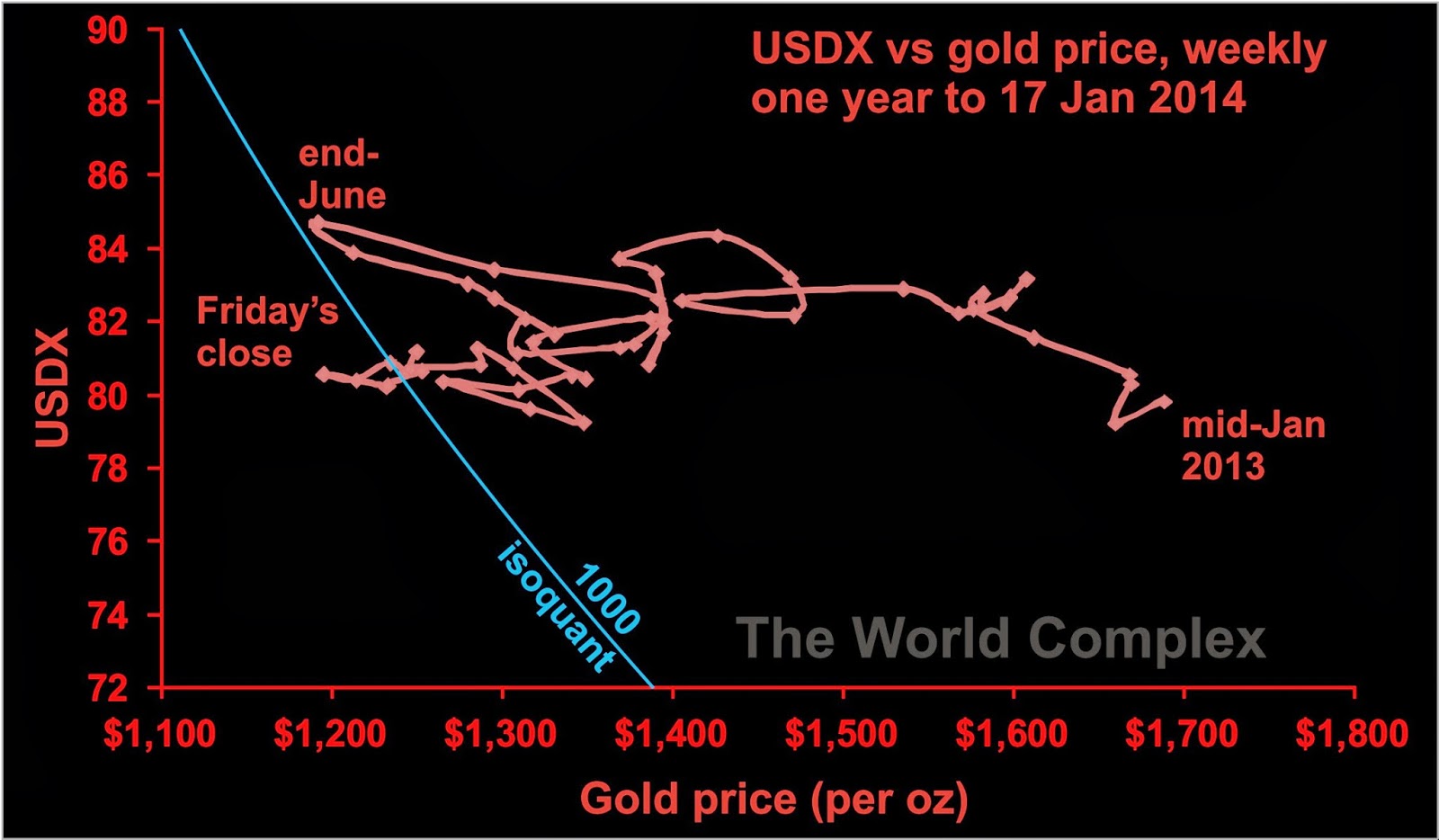

The last year has consisted of a dizzying drop in the price of gold, a bounce in mid-summer and a lot of hard work in the last six months. The rapid fall in early 2013 bounced from the 1000 isoquant. There was a second small bounce in October, followed by a slight penetration of the 1000 isoquant last month. Friday's close is just above the 1000 isoquant.

The last time the gold x USDX was near the 1000 isoquant was in 2010, when it stayed there for nearly six months. Note that even though gold x USDX was nearly constant for that time, the gold price itself varied from less than $1200 to over $1350. This is the way we normally expect the price of gold to act--as the anti-dollar.

Over the last six years, sustained improvements in gold x USDX require the gains be digested for a time. Usually we see six or so months at one isoquant, before a move to a new one 100-150 points higher, which then needs six months or so before another move is sustainable. When gold spiked to $1800 in 2011, gold x USDX moved from just over 1100 to just over 1400 in too short a time--the result was the collapse we have just lived through back to the 1000 isoquant.

The significance of the isoquant is that changes in the price of gold that are offset by changes in the US dollar do not change the marginal economics of gold mine operations (that is costs in the country of operation, provided it is not the US). They do influence the ability of the company to repay debt, which is normally denominated in US dollars--however, many (I don't know if it is all) loan covenants include a gold-hedging component which in theory reduces the dollar risk to the producer. The company then only has to worry about producing x hundred thousand ounces of gold each year (if they can't deliver on their promises, well, that's another problem).

The last year has consisted of a dizzying drop in the price of gold, a bounce in mid-summer and a lot of hard work in the last six months. The rapid fall in early 2013 bounced from the 1000 isoquant. There was a second small bounce in October, followed by a slight penetration of the 1000 isoquant last month. Friday's close is just above the 1000 isoquant.

The last time the gold x USDX was near the 1000 isoquant was in 2010, when it stayed there for nearly six months. Note that even though gold x USDX was nearly constant for that time, the gold price itself varied from less than $1200 to over $1350. This is the way we normally expect the price of gold to act--as the anti-dollar.

Over the last six years, sustained improvements in gold x USDX require the gains be digested for a time. Usually we see six or so months at one isoquant, before a move to a new one 100-150 points higher, which then needs six months or so before another move is sustainable. When gold spiked to $1800 in 2011, gold x USDX moved from just over 1100 to just over 1400 in too short a time--the result was the collapse we have just lived through back to the 1000 isoquant.

The significance of the isoquant is that changes in the price of gold that are offset by changes in the US dollar do not change the marginal economics of gold mine operations (that is costs in the country of operation, provided it is not the US). They do influence the ability of the company to repay debt, which is normally denominated in US dollars--however, many (I don't know if it is all) loan covenants include a gold-hedging component which in theory reduces the dollar risk to the producer. The company then only has to worry about producing x hundred thousand ounces of gold each year (if they can't deliver on their promises, well, that's another problem).

Excellent simplified expansion for my simple mind. Thank you. Further work, as you choose, would be appreciated.

ReplyDeleteOff-topic, but I believe relevant to your interests and analytical methodologies as demonstrated:

Nodal instability in the financial system (2009)

Re: www.imsc.res.in/.../Sinha_Are_complex_financial_systems...

Financial Markets are Complex Systems ! ... Complex markets are unstable As the interaction between agents increase in complexity ... state of the ithth node.node...

http://www.imsc.res.in/~sitabhra/talks/Sinha_Are_complex_financial_systems_stable_IISc_11_2011.pdf

Apologies for poor editing; the pdf is IMO excellent.

There was a paper by Battiston et al. (included Stiglitz) that I reviewed earlier that covers similar ground. The review has a link to the original pdf. http://worldcomplex.blogspot.ca/2012/02/another-view-on-default-cascades.html

DeleteGiven that a significant basis for the above post, mm, is the marginal economics of gold mine operations, it would seem appropriate and meaningful to apply such methodologies to the HUI as well as the Comex "price" of gold. As you well know, producer forward hedging has diminished materially over the last 4 years, but may have re-emerged for specific purposes within the last 6 months due to marginal and total physical market tightness. Perhaps I am incorrect...reply would be appreciated.

ReplyDeleteThere is one I have that predates the isoquant business, where I just considered the value of gold price x USDX, and compared it with the GDX.

Deletehttp://www.worldcomplex.blogspot.ca/2013/12/gold-usdx-breaks-down.html

Antal Fekete wrote some articles several years ago discussing the appropriate use for gold hedging by mining companies. The gist of his argument was that, used properly, they allowed the company to maximize gold recovery from a particular mine. Unfortunately, in the late 90s, many companies used them as a way to speculate on continued declines in the gold price and so got into trouble (Ashanti, Barrick).